Getting Started With Evaluating Mutual Fund Performance

Internal Fund Expenses. In addition to the load you might be paying, you’re also paying internal expenses that go toward the operation and management of the specific mutual fund. Without going into all of the different types of mutual funds, the general principle is that you tend to pay more for an active portfolio manager monitoring a mutual fund, and you tend to pay less for a fund with a passive investing strategy, such as an index fund. One type isn’t necessarily better than the other, but again, I believe that a general guideline for what you’re willing to pay is reasonable—for example, most of my clients tend to stay at 1% or below. You can check and see how much your mutual fund is charging you, typically under the heading of “Expenses” on the fund fact sheet.

Internal Fund Expenses. In addition to the load you might be paying, you’re also paying internal expenses that go toward the operation and management of the specific mutual fund. Without going into all of the different types of mutual funds, the general principle is that you tend to pay more for an active portfolio manager monitoring a mutual fund, and you tend to pay less for a fund with a passive investing strategy, such as an index fund. One type isn’t necessarily better than the other, but again, I believe that a general guideline for what you’re willing to pay is reasonable—for example, most of my clients tend to stay at 1% or below. You can check and see how much your mutual fund is charging you, typically under the heading of “Expenses” on the fund fact sheet.

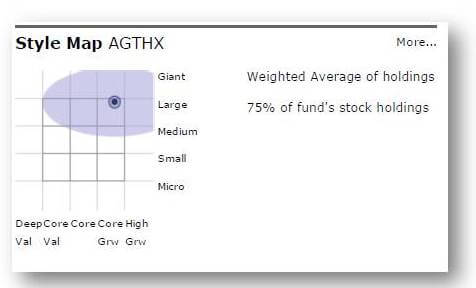

Asset Class. Asset class simply refers to what “flavor” of mutual fund you’re purchasing, and all of them are initially categorized by the size of the company and phase of growth. Ideally, small, medium and large companies would move differently—if one class is up, another would be down, and so on. We can’t control that, but diversification is still important, which is why I encourage people to make sure they spread out their investments over multiple asset classes, which they can check for by looking at the individual fund’s style box.

Asset Class. Asset class simply refers to what “flavor” of mutual fund you’re purchasing, and all of them are initially categorized by the size of the company and phase of growth. Ideally, small, medium and large companies would move differently—if one class is up, another would be down, and so on. We can’t control that, but diversification is still important, which is why I encourage people to make sure they spread out their investments over multiple asset classes, which they can check for by looking at the individual fund’s style box.

One mistake I see often is that someone has invested in multiple mutual funds—perhaps in their 401(k)—but the underlying holdings are identical. Every fund will tell you what their Top Holdings are, so you need to compare and make sure your funds aren’t in 3 different funds with identical holdings! You’ll see below I compared two American Funds, and both of them have Apple and tobacco companies, so they may not be the best funds to hold together if you’re looking for diversification.

One mistake I see often is that someone has invested in multiple mutual funds—perhaps in their 401(k)—but the underlying holdings are identical. Every fund will tell you what their Top Holdings are, so you need to compare and make sure your funds aren’t in 3 different funds with identical holdings! You’ll see below I compared two American Funds, and both of them have Apple and tobacco companies, so they may not be the best funds to hold together if you’re looking for diversification.

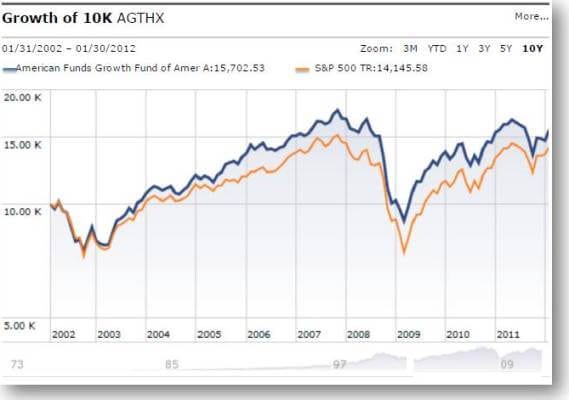

Benchmark. The final checkpoint for evaluating your mutual fund is to compare it to other similar entities—every single asset class has a corresponding index, which you can use to see how the overall asset class is performing, and then see how your individual mutual fund is holding up against that benchmark. Often when you pull up your mutual fund’s information, a benchmark is already provided for comparison. The question they are answering with the below chart is, if you invested $10,000, how has the benchmark and your mutual fund performed over the same timeframe?

Benchmark. The final checkpoint for evaluating your mutual fund is to compare it to other similar entities—every single asset class has a corresponding index, which you can use to see how the overall asset class is performing, and then see how your individual mutual fund is holding up against that benchmark. Often when you pull up your mutual fund’s information, a benchmark is already provided for comparison. The question they are answering with the below chart is, if you invested $10,000, how has the benchmark and your mutual fund performed over the same timeframe?

As you can see, this specific mutual fund (blue) did better than its benchmark (orange) during the 10-year timeframe. Although, if it even simply held even with the benchmark, I would still be satisfied . . . it’s only when you can see consistent performance below the benchmark that you need to look at making a change.

When it comes to mutual fund investing and evaluating performance, the multitude of criteria can become very confusing very quickly--and there is A LOT here that I haven't mentioned that sophisticated investors may factor into their evaluation process. However, many people lose sight of what they are trying to accomplish when confronted with too much data and become paralyzed! With these four simple guidelines, you can get started on the road to understanding your mutual fund investments more easily, while maintaining your forward long-term investing momentum.

As you can see, this specific mutual fund (blue) did better than its benchmark (orange) during the 10-year timeframe. Although, if it even simply held even with the benchmark, I would still be satisfied . . . it’s only when you can see consistent performance below the benchmark that you need to look at making a change.

When it comes to mutual fund investing and evaluating performance, the multitude of criteria can become very confusing very quickly--and there is A LOT here that I haven't mentioned that sophisticated investors may factor into their evaluation process. However, many people lose sight of what they are trying to accomplish when confronted with too much data and become paralyzed! With these four simple guidelines, you can get started on the road to understanding your mutual fund investments more easily, while maintaining your forward long-term investing momentum.Article author

About the Author

Further reading

Further Reading

Article

The ROI of Loyalty: Measuring Dealership Rewards Success

In todayâs competitive automotive market, a sale isnât the end of the roadâitâs just the beginning. For dealerships, building long-term relationships with customers is essential, and one of the most effective tools in achieving this is a well-designed loyalty program. But how do you know if your investment in a Dealership Rewards Programs is paying off? Letâs explore how forward-thinking dealerships measure the ROI of loyalty and turn repeat customers into raving fa

November 28, 2025

Article

Top 10 Finance Apps for Your Phones

Take Care of All Your Financial Organization With These Great AppsrnLiving in the 21st century provides plenty of exciting new financial opportunities. You can do all your banking through the internet, get fast cash through Online Title Loans and even apply for 2nd lien title loans through an online application. And, of course, more apps are coming out every day that can help you better manage your money and make it grow. Here are 10 of the top finance apps you can get on you

May 13, 2024

Article

Powering Your Home and Your Wallet: How to Finance Your Solar Installation

Harnessing the sun's energy with solar panels can be a fantastic investment, but the upfront cost can seem daunting. Thankfully, various financing options can help you make the switch to solar without breaking the bank. This article explores the main ways to finance your solar installation, empowering you to choose the best path for your financial situation. Understanding Your Options: Before diving into specifics, it's crucial to understand the two main ownership models: Own

February 16, 2024

Article

Unlock Fast Cash with Texas Car Title Loans: Experience Quick Approval Online

In the pursuit of financial solutions, speed is often crucial. Texas Car Title Loan brings you the convenience of fast approval online title loans, providing quick and easy access to the cash you need. Explore the world of Texas car title loans for same-day solutions that ensure your financial needs are met promptly. Fast Approval Online Title Loans: The Key to Quick Cash When urgent financial needs arise, waiting for funds can be stressful. Our fast approval Online Title Loa

December 13, 2023